Exhibit A: Case #002 | The account that became a risk

Daniel Park woke before the alarm because the radiator had started its old mechanical sermon again. The pipes in the apartment building always knocked before dawn in winter, as if the heat had to fight its way floor by floor through fifty years of rust and repainting. Metal expanded inside the walls with hollow little strikes that sounded like someone tapping a wrench against a courthouse rail. Daniel lay still for a moment, staring at the pale ceiling while the room slowly took on the weak gray light of February.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

The apartment was quiet enough for him to hear his mother moving in the kitchen.

Not walking, exactly. Slippers dragging. Cabinet opening. Closing. Opening again.

He threw back the blanket and crossed the cold hardwood in his socks.

His mother stood at the counter in her robe, looking down at the toaster as if she had found it in someone else’s home.

“Omma?”

She turned toward him with that brief startled look he had come to hate, the tiny flash of uncertainty before she recognized his face.

“There you are,” she said, relieved. “I was looking for the tea.”

“It’s right here.”

He reached past her gently, took down the dented tin from the upper shelf, and set it beside the kettle. Her hands had once moved through kitchens with effortless authority. She had cooked for six on holidays in a space smaller than this one. Now she sometimes stood in front of the stove and forgot which knob controlled which flame.

“You’re up early,” she said.

“So are you.”

“I have to get ready.”

Daniel looked at her for a second.

“For what?”

She smiled faintly, not embarrassed, not yet confused, simply drifting. “You said we were going somewhere.”

He had said that, last night, because it was easier than explaining memory care in words that felt like betrayal.

“We are,” he said. “Later this morning.”

She nodded as if that confirmed something she had already decided. Then she touched the kettle, found it cold, and looked at him again. “Your father liked tea before a trip.”

The sentence landed softly between them.

His father had been dead for eleven years.

Daniel took the kettle from her hand. “I’ll make it.”

By the door sat the blue overnight bag.

He had packed it after midnight, kneeling on the living room rug while his mother slept in the recliner with the television murmuring to itself. The bag was old, canvas faded at the seams, one zipper tab replaced with a brass key ring. It had once belonged to his parents. Daniel remembered it in motel rooms, in summer cabins, in the trunk of his father’s Buick on drives that felt endless when he was a child. Now it held two cardigans, thick socks, slippers, her blood pressure pills, the framed church photo she liked on the side table, and the small quilt she insisted was warmer than any blanket anyone made now.

Beside the bag lay a cream-colored folder from Juniper House Memory Care.

His name was on the intake documents.

His mother’s name was on the residency agreement.

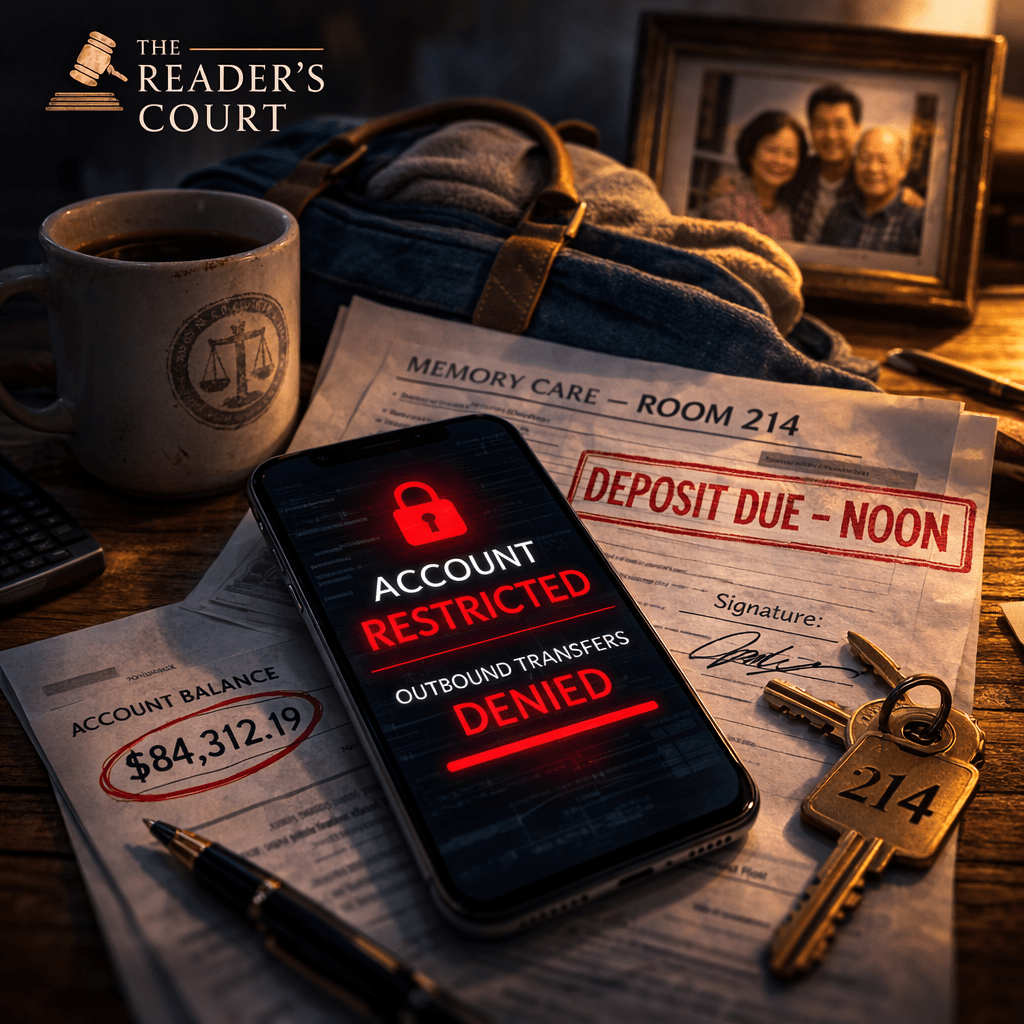

A room number had finally been assigned yesterday afternoon.

Room 214. Garden side.

He had waited seven months for that call.

Seven months of telling himself he could still manage. Seven months of taking calls from neighbors who had found his mother in the hallway, in the laundry room, once outside in the courtyard in house slippers asking a delivery driver whether he knew the way back to Flushing. Seven months of pretending that the burn mark on the saucepan meant only that she had been tired, not that she had turned on the stove and walked away.

Juniper House had one room open because another family, the coordinator told him in a voice practiced enough to be both kind and efficient, had declined when they saw the price.

If Daniel wanted it, they needed the deposit wired by noon.

Noon.

He had repeated the word back to her as though hearing it twice might make it less sharp.

Now the folder sat on the narrow table under the window, neatly squared beside the transfer instructions and a black pen. He had reviewed everything three times before bed. He had enough in the account. Not enough for comfort, not enough for mistakes, but enough. He could send the deposit before work, sign the admission papers, and move her in by afternoon before the place gave the room to the next family on the waiting list.

His mother carried her mug to the table and sat down slowly.

“Are we going far?” she asked.

“No.”

“Overnight?”

Daniel glanced at the blue bag by the door.

“Maybe for a little while.”

She looked down into her tea. “I don’t want to be any trouble.”

He sat across from her. “You’re not trouble.”

“You say that too fast.”

He almost smiled.

Some part of her still had perfect aim.

He reached for his coffee mug, the old white one with the faint courthouse seal worn nearly away from years of dish soap and use. Someone had given it to him after a trial his second year as a public defender, back when he still believed good work earned protection from the machinery around it. The mug was chipped at the rim. He used it every morning anyway.

His phone buzzed against the table.

An email notification lit the screen.

Security Notice: Account Status Update.

Daniel frowned but did not open it immediately. He had too much to do this morning, too many fragile things already lined up in his head. Instead he slid the phone aside and said, “Drink your tea. Then I’ll help you get dressed.”

His mother nodded. “Should I wear the green sweater?”

“The dark one?”

“Yes.”

“That one’s good.”

She gave him a small, satisfied look, as if they had solved something ordinary together.

He helped her back to the bedroom, laid the green sweater across the bed, and set out her slacks and soft-soled shoes. On the dresser stood the framed photograph he had packed a duplicate of for the new room: his parents on a picnic blanket in 1989, his mother leaning into the wind, his father squinting at the camera, Daniel himself small and solemn between them in a baseball cap too large for his head.

He stood there longer than he meant to.

Then he returned to the kitchen table, opened the banking app, and prepared to send the wire.

For one second the screen looked normal.

Checking account.

Available balance.

Then the number sharpened into view and Daniel’s hand stopped.

$84,312.19

He stared at it.

That was wrong.

Very wrong.

Yesterday evening the balance had been just over six thousand dollars. Tight, but enough. He had checked it twice while calculating what would remain after the deposit. He knew the number with the defensive intimacy of a man who had spent months moving money in careful inches.

He opened the transaction list.

At the top sat a posting from 11:47 p.m.

Incoming Wire Transfer — $78,000.00

Sender: Evan Rourke

Daniel looked at the name as though it belonged to someone from a previous life.

Rourke.

Law school years. Cheap beer. Big plans. Then the brief detour Daniel never took—the startup Rourke had tried to build, the one Daniel almost joined before deciding law school debt was already enough of a gamble. After that they drifted. Christmas cards for a while. Then nothing.

His mother called faintly from the bedroom. “Daniel?”

“Yeah?”

“Where are my earrings?”

“In the top drawer.”

He did not take his eyes off the screen.

A red banner spread across the top of the app like a warning light.

ACCOUNT RESTRICTED

Below it, smaller text appeared.

Outbound transfers temporarily unavailable.

Daniel tapped the wire transfer icon anyway.

The app answered instantly.

Action unavailable under current account status.

He set the phone down and picked it up again. His body had already gone cold under the skin. The room seemed to flatten around him. The blue overnight bag by the door. The cream folder on the table. The courthouse mug cooling beside his hand. All of it suddenly arranged inside a world he no longer controlled.

He opened the email.

Your account has been temporarily restricted due to a risk evaluation conducted under our automated compliance program.

Certain features may be unavailable while the review is in progress.

For additional information, please contact customer support.

He called the number.

The menus took forever because every second inside an automated voice feels designed to prove you are not the emergency. He entered the last four digits of his social, confirmed the account, chose checking, chose online access, chose “other,” and listened to a piano version of some song he could not identify.

From the bedroom, dresser drawers opened and closed. His mother hummed to herself.

A representative finally answered with the tired brightness of someone at the beginning of a long day.

“My account has been restricted,” Daniel said. “I need to send a wire this morning.”

“One moment while I review the account, sir.”

He stared at the red banner on the app while she typed.

“Thank you for waiting. Your account has been flagged under our automated compliance monitoring system.”

“Flagged for what?”

“I’m afraid I can’t see the specific category.”

“I need to move money now. Not next week. This morning.”

“I understand.”

“No, you don’t. There’s a deposit due at noon.”

Another pause. “Reviews may take up to thirty business days.”

Daniel laughed once, without humor.

“That’s six weeks.”

“Yes, sir.”

“That’s not a review. That’s a seizure.”

“I’m sorry for the inconvenience.”

He looked at the bag by the door. He looked at the folder. Through the open bedroom door he could see the sleeve of the green sweater laid across the bed exactly where he had placed it.

He lowered his voice because anger in front of his mother now felt like another kind of failure.

“An incoming wire hit my account last night. I didn’t request it.”

“I do see a recent incoming transfer.”

“From Evan Rourke.”

She said nothing.

Daniel opened his laptop with one hand and typed the name into the search bar. Results populated before he finished the surname.

The first headline was eight months old.

FINANCIAL ANALYST DISAPPEARS DURING FEDERAL INVESTIGATION

He clicked it.

Rourke’s face appeared on the screen, older and heavier than Daniel remembered, but unmistakable. The article described suspected movement of funds across offshore accounts tied to a corporate fraud inquiry. Investigators had wanted to question him. Instead he disappeared.

Daniel felt the blood drain from his face.

“Your system thinks I’m part of this?” he asked.

“Sir, I’m not able to confirm the precise nature of the alert.”

“But it can lock my account.”

“Our systems monitor activity associated with financial risk.”

“My mother has a room waiting for her.”

The words came out before he could stop them.

There was a silence on the line then, the terrible sterile silence of a person who hears the human fact but has no place to put it.

“I’m sorry,” the representative said softly. “I cannot override the restriction.”

His mother appeared in the doorway wearing the green sweater and only one earring.

“How do I look?” she asked.

Daniel turned in his chair.

Beautiful, he wanted to say.

Like yourself.

Like the part of this life I am trying not to lose by inches.

Instead he smiled with effort. “You look good. The other earring is on the dresser.”

She touched one ear, surprised to find it bare. “Your father always noticed first.”

Daniel swallowed.

On the phone the representative was still speaking, but the words no longer mattered. Escalation queue. Security team. Review process. He heard them as if from underwater.

His mother came closer to the table and looked at the folder, then at the blue bag.

“Are we late?” she asked.

Daniel opened the app again because some part of him still believed screens could be persuaded by repetition.

The balance remained.

The wrong money remained.

The red banner remained.

ACCOUNT RESTRICTED

His thumb hovered over the transfer icon. He pressed it once more, not because he expected mercy, but because human beings are slow to surrender when a promise is sitting in a blue canvas bag by the door.

The screen flashed and answered him in hard, instant text.

Outbound transfers temporarily unavailable.

Become a member of the Dossier.

Support my writing.

The Question | The Account That Became a Risk

Daniel Park did not solicit the money. He did not hide it, spend it, reroute it, or even understand it until it was already sitting inside his account.

He woke up as the same law-abiding customer he had been the night before, with the same six thousand dollars he had saved, the same mother who needed a room by noon, and the same intention any ordinary person would recognize as decent: keep her safe.

Then an automated system fused his money to someone else’s suspicion and converted access into a privilege that could be withdrawn without warning.

So what exactly happened in that moment?

How does a lawful customer become a risk category before he becomes a person anyone is required to listen to?

The Autopsy | The Account That Became a Risk

What happened to Daniel Park sits inside the architecture of modern anti-money-laundering enforcement, where banks are expected to identify suspicious activity quickly, isolate it quickly, and document it quickly. The relevant systems do not wait for a criminal conviction. They do not require courtroom standards. They operate on patterns, counterparties, transaction histories, behavioral deviations, and associations that suggest possible exposure.

An incoming wire from a person connected to prior investigative scrutiny is the kind of event these systems are built to catch. Once that happens, the account may be restricted automatically or pushed into a review state that functionally produces the same result. Front-line employees often cannot see the underlying trigger, and even when they can infer it, they are trained not to say much. Some of that silence is procedural. Some of it is legal. Some of it exists because transparency creates its own form of institutional risk.

This is the part ordinary customers rarely understand: the bank is not asking whether Daniel Park is morally innocent in the human sense. It is asking whether his account now presents regulatory, reputational, or financial exposure to the institution. Those are different questions.

The bank’s incentives are not arranged around the customer’s immediate life. They are arranged around avoiding supervisory penalties, preserving access to payment networks, satisfying compliance obligations, and preventing the kind of scrutiny that can produce massive fines, legal costs, damaged investor confidence, and restrictions on future business. In that environment, a false positive imposed on one customer is cheaper than a false negative imposed on the bank.

So the burden shifts silently downward.

Daniel loses access to his own lawful funds because the institution would rather immobilize him than risk appearing permissive toward suspicious money. His mother’s room, his deadline, his promise, his circumstances—none of that enters the primary calculation. The human question is, What is right here? The institutional question is, What most safely protects the bank?

No villain is required for this to happen. The representative can be polite. The model can be functioning as intended. The rules can be followed carefully at every step. That is precisely what makes the mechanism so cold. Integrity, decency, and moral proportion are not removed in a dramatic act. They are simply absent from the design priority.

And that design priority ultimately serves concentrated wealth. A large financial institution protects itself first because its real exposure is not one customer’s hardship. Its exposure is regulatory force, market confidence, and the stability of the capital structure above the customer. When those interests conflict, the ordinary account holder absorbs the delay, the opacity, and the loss.

The Reader’s Verdict | The Account That Became a Risk

The money appeared.

The model saw the wrong pattern attached to the wrong name and made the safer choice for the institution.

It did not matter that Daniel Park wanted only to move his own six thousand dollars. It did not matter that a room was waiting. It did not matter that his mother had already put on the green sweater.

His account was not judged by what he needed.

It was judged by what the bank feared.

That is the quiet truth beneath the polite language of review.

The system did not fail.

It simply answered the question it was designed to answer.

And in systems designed to protect institutional power and wealth, integrity, decency, and morality rarely appear in the calculation.

FILE YOUR VERDICT — The Account That Became a Risk

What is the right thing to do?

A) Restrain first contact. Suspicious incoming wires should be quarantined at the edge: the bank can hold the new money, but it should not freeze a customer’s existing funds or block time-critical obligations.

B) Restrain escalation. If an account is restricted, the bank must provide an emergency human review path and a hardship release for essentials (elder care, medical, housing) with a short clock—days, not “up to thirty business days.”

C) Fix the system. Pass a financial-integrity package: binding transparency at least to the category level, strict time limits on freezes without a court order, independent appeal/ombudsman review, and enforceable accountability for false-positive harm—so “compliance” can’t function as a polite seizure.

Choose your verdict: A, B, or C.

Then comment in one sentence: what cost are you willing to accept to make your choice real?

—Mark Bertrand

The Reader’s Court

When systems break people’s lives, the truth must be told.

Join the fight.

0 comments

Write a comment